Chinese E-Commerce Businesses Moving West - 中國電商向西發展

Director 指揮 : KEITH YUNXI ZHU 朱耘希 | IVY YI REN 仁一

Supervisor 監視 : Oliver Thomas Dalmi 達爾米 托馬斯 奧立佛

Authors 作者 : Yuhan Kang, Jingyang Wu, Haoyan Liu, Benjamin Duncan

In June and July of 2021, TKEG Expat (China) served around 50 Chinese E-Commerce Businesses that wanted to set up subsidiaries in Ireland to avoid Amazon's tax declaration change in July. TKEG discovered that many clients did not understand the European Tax System and Amazon’s tax declaration scheme, therefore caused misunderstood that which Ireland would be the ideal destination.

在2021年六月及七月,奕資環球(中國)為大約50家中國電子商務企業提供服務,這些企業希望在愛爾蘭設立子公司,以避免亞馬遜7月份的納稅申報變更。奕資發現許多客戶不瞭解歐洲稅收體系和亞馬遜的納稅申報方案,囙此導致了對愛爾蘭是理想目的地的錯誤認知。

BACKGROUND BRIEF

背景提要

In June and July, TKEG Expat (China) served around 50 Chinese E-Commerce Businesses that wanted to set up subsidiaries in Ireland to avoid Amazon's tax declaration change in July. TKEG discovered that many clients did not understand the European Tax System and Amazon’s tax declaration scheme, therefore caused misunderstood that which Ireland would be the ideal destination.

在六月及七月,奕資環球(中國)為大約50家中國電子商務企業提供服務,這些企業希望在愛爾蘭設立子公司,以避免亞馬遜7月份的納稅申報變更。奕資發現許多客戶不瞭解歐洲稅收體系和亞馬遜的納稅申報方案,囙此導致了對愛爾蘭是理想目的地的錯誤認知。

1

Chinese-European E-commerce History

中歐電商歷史

Background of "One Belt, One Road"

一帶一路的背景

The connection between China and European countries along OBOR mainly relies on the China-EU Railway. The China-EU Railway will operate in accordance with fixed train numbers, routes and schedules, and will mainly travel between China and major cities in European countries along OBOR, such as Madrid and Hamburg. The running time of this train is three-quarters less than that of sea transportation, and the price is about one-fifth of aerial transportation. It can conveniently transport commodities such as bulk electronic goods, light industry and high-tech electronic products, thus strengthening China's commercial and trade ties with European countries [4]. As of the end of 2019, China-Europe freight trains had operated 8,225 trains, a year-on-year increase of 29%, and 725,000 TEUs were shipped, a year-on-year increase of 34% [2]. At the same time, China's opening cities have increased to 71 in May 2020, 2.5 times the number in 2017. In addition, the number of connected cities in Europe has increased from 29 cities in 11 countries in 2017 to 67 cities in 19 countries in 2020 [3]. It can be seen that the logistics organization of China-EU Railway has become increasingly mature and has become an inseparable part of international logistics land transportation.

一帶一路與歐洲國家的對接主要依賴於中歐班列。中歐班列將按照固定車次、線路及班期開行,主要來往於中國和一帶一路沿線的歐洲國家的主要城市,比如馬德里、漢堡等。該班列的運行時間比海運節省四分之三,而價格約為航空的五分之一,能夠便利地對大宗電子商品、輕工及高科技電子產品等商品進行運輸,從而加強了中國與歐洲國家的商業貿易聯絡 [4]。截至2019年底,中歐班列開行8,225列,同比增長29%,發運了72.5萬標準箱,同比增長34% [2]。同時,2020年5月的中國開行城市增加到了71個,是2017年的2.5倍。除此之外,對接的城市也從2017年的11個國家29座城市增加到了2020年的19個國家67座城市 [3]。由此可見,中歐班列物流組織日趨成熟,已經成為了國際物流陸運運輸不可分割的一部分。

China has also begun infrastructure investment and construction in Southeastern Europe to build the "Balkan Silk Road". The "Balkan Silk Road" will enable China to achieve closer connections with major cities in Southeastern European countries such as Greece, Serbia, and Bosnia and Herzegovina, and give China a more convenient channel to Central European countries. In August 2016, China Ocean Shipping Company has acquired a 51% stake in the Greek Port of Piraeus [6], which is one of the largest container ports in the central Mediterranean region. After the acquisition, the port will play a vital role in the transportation of goods by sea and land along OBOR and become the core of the "Balkan Silk Road". It is predicted that China's investment will achieve significant results within ten years. 10% of China's exports to Europe will pass through the port of Piraeus [5], enabling the "Balkan Silk Road" to drive the development of Southeastern European countries and reduce logistics costs between China and Europe. In summary, the "Balkan Silk Road" will open up a new and convenient route for China's exports to Europe and the import of European goods.

中國也開始在東南歐地區開始了基礎設施的投資與建設,以此構建 “巴爾幹絲綢之路”。“巴爾幹絲綢之路”將會使中國與希臘、塞爾維亞、波黑等東南歐國家的大城市實現更為緊密的連結,給予中國一個更為便捷的通往中歐國家的通道。2016年8月,中國遠洋運輸公司已經收購了希臘的比雷埃夫斯港的51%的股份 [6],該港口是地中海中部地區最大的集裝箱港口之一。收購之後,該港口將承接從一帶一路沿線發出的海陸聯運貨物,成為 “巴爾幹絲綢之路” 的核心。預測估計,中國的投資將在十年之內取得顯著成果。中國出口歐洲的產品將會有10%通過比雷埃夫斯港 [5],使得 “巴爾幹絲綢之路” 帶動東南歐國家的發展,同時降低中歐之間的物流成本。綜上所述,“巴爾幹絲綢之路” 將會為中國對歐洲出口和歐洲商品的輸入開闢一條新的便捷航線。Active Chinese E-commerce industry

活躍的中國電商

Although the Covid-19 pandemic in 2020 has had a significant impact on the global economy, the total global B2C cross-border e-commerce trade has shown an increasing trend. According to a WTO report, the total amount of B2C cross-border e-commerce trade will grow from US$780 billion in 2019 to US$4.8 trillion in seven years, with a compound growth rate of 27%. The import and export of China's cross-border e-commerce is also showing a growth trend in 2020. According to data from China Customs, China's cross-border e-commerce imports and exports increased by 31.1% to a total of 1.69 trillion yuan. Among them, the total export value was 1.12 trillion yuan, an increase of 40.1% [7].

雖然2020年的新冠疫情對全球經濟造成了重大影響,全球B2C跨境電商貿易總額去呈現了增長趨勢。根據世貿組織的一份報告,B2C跨境電商貿易總額將在七年內從2019年的7,800億美元增長到4.8萬億美元,復合增長率將高達27%。中國跨境電商的進出口也在2020年呈現了增長趨勢。根據中國海關的數據,中國跨境電商的進出口增長了31.1%,總額為1.69萬億元。其中出口總額為1.12萬億元,增長40.1% [7]。

The overseas business market of China's e-commerce can be divided into two tiers. The tiers are divided according to the country's frequency of appearance in the top ten rankings of gross merchandise value in the past ten years. The first tier includes the United States, Russia, France, Spain, etc. The second tier includes Poland, Ukraine, South Korea, Israel, etc. [7]. It can be seen that the overseas business markets of Chinese e-commerce companies are mainly concentrated in developed countries such as the United States and those in Europe.

中國電商的海外業務市場可以分為兩個梯隊,梯隊是按照過去十年該國家在成交總額前十排名中的出現頻率來劃分的。第一梯隊為美國、俄羅斯、法國、西班牙等。第二梯隊為波蘭、烏克蘭、韓國、以色列等 [7]。由此可見,中國電商的海外業務市場主要集中在美國和歐洲等發達國家。

Through OBOR, China has achieved closer economic ties with countries along the route. AliExpress big data shows that since 2011, countries along OBOR have accounted for 38% of the countries that appeared in the top ten rankings in terms of gross merchandise value. At the same time, Alibaba's cross-border e-commerce big data shows that Eastern European countries are one of the groups most closely connected with China's cross-border e-commerce. Moreover, in the context of the US-China trade war, the proportion of China's cross-border e-commerce major exporting countries has changed significantly. The United States has decreased from 17.50% in 2018 to 15.00% in 2019, and France has decreased from 13.20% to 11.40%. At the same time, Russia has increased from 11.30% to 12.50%. The total proportion of other Central European, Eastern European and East Asian countries increased from 44.00% to 45.90% [7]. It can be seen that the implementation of OBOR and changes in the international political background provide favorable opportunities for the development of Chinese e-commerce in Europe. The irreversible nature of these two major trends also means that the proportion of emerging markets in Europe will only increase among the exporting countries of China's e-commerce. In summary, China's cross-border e-commerce business is expected to maintain growth momentum in Russia, Spain and other countries, while maintaining a lot of room for growth in countries with relatively poor infrastructure in Central and Eastern Europe.

受到一帶一路的影響,中國與沿線各國取得了更為緊密的經濟聯繫。全球速賣通大數據顯示,自2011年以來,一帶一路沿線國家在進入成交總額前十的國家中佔比38%。同時,阿里巴巴跨境電子商務大數據顯示,東歐國家是與中國跨境電商連結最為緊密的群體之一。而且,在中美貿易戰的背景下,中國跨境電商主要出口國家佔比有了顯著的變化。美國從2018年的17.50%下降到了2019年的15.00%,法國從13.20%下降到了11.40%。同時,俄羅斯從11.30%上升到了12.50%。而其他中歐、東歐及東亞國家的總佔比從44.00%上升到了45.90% [7]。由此可見,一帶一路倡議的實施與國際政治背景的變動為中國電商在歐洲的發展提供了有利的契機。這兩個大趨勢不可逆轉的性質也意味著歐洲的新興市場的佔比將在中國電商出口國家之中只增不減。綜上所述,中國跨境電商的業務有望在俄羅斯、西班牙等國家保持增長勢頭,同時也在中東歐基礎設施相對差的國家保持很大的增長空間。

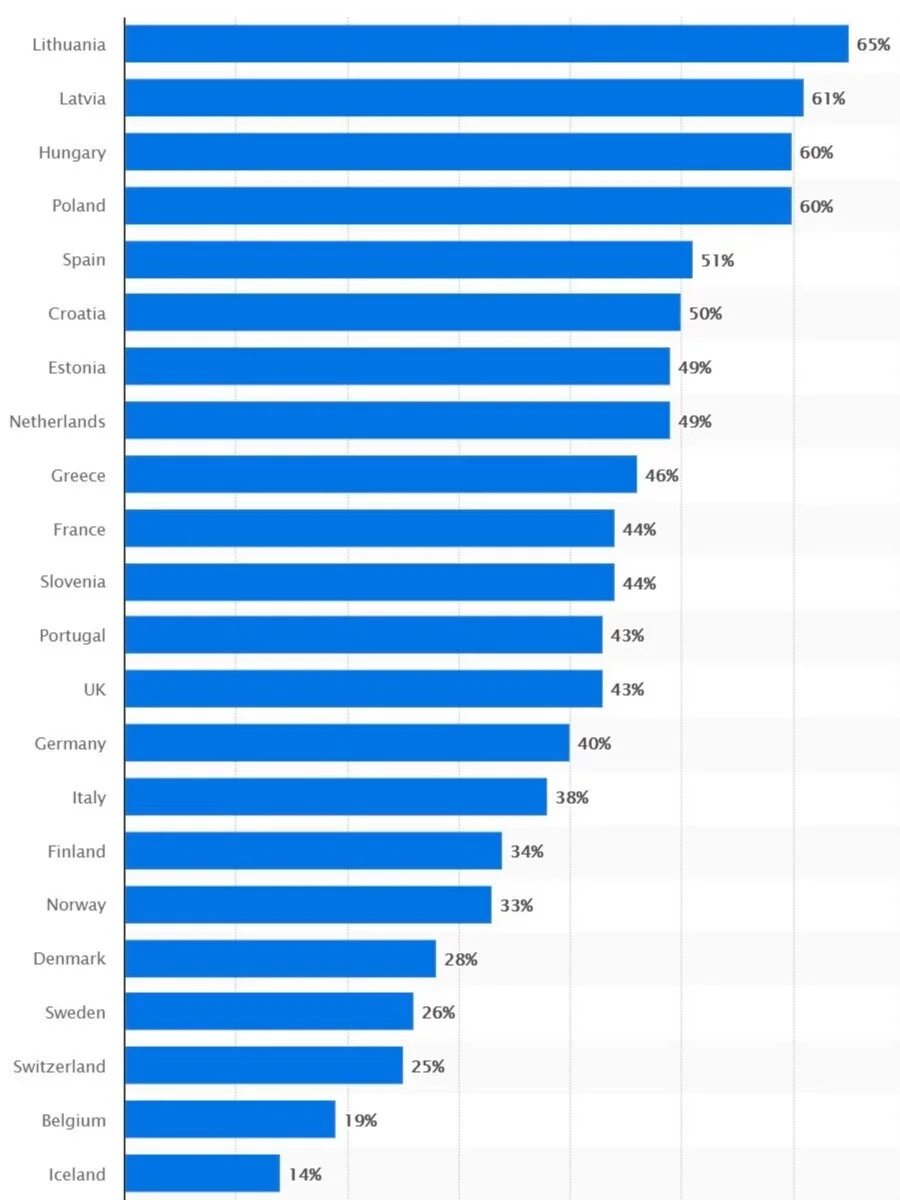

The plot shows share of people in Europe who bought their most recent online cross-border purchase from China as of October 2020, by country.

此圖顯示了截至 2020 年 10 月,按國家/地區劃分的歐洲人最近一次從中國在線跨境購物的比例。

As we can see, people in East-Europe countries rely more on Chinese product, in contrast to the lower percentage in West and South Europe. The percentage of usage of online shopping to buy products from China in some countries are surprisingly high, such as 63% in Lithuana, 61% in Latvia and 60% in both Hungary and Poland. More developed countries, such as Sweden and UK, spend less on Chinese product, while the reasons may be complicated, including but not limited to politics and the ability and cost of producing goods locally.

正如我們所看到的,東歐國家的人們更多地依賴中國產品,而西歐和南歐國家的人口比例較低。 一些國家使用網購購買中國產品的比例高得驚人,例如立陶宛為 63%,拉脫維亞為 61%,匈牙利和波蘭為 60%。 瑞典、英國等較發達國家在中國產品上的支出較少,原因可能很複雜,包括但不限於政治以及在當地生產商品的能力和成本。

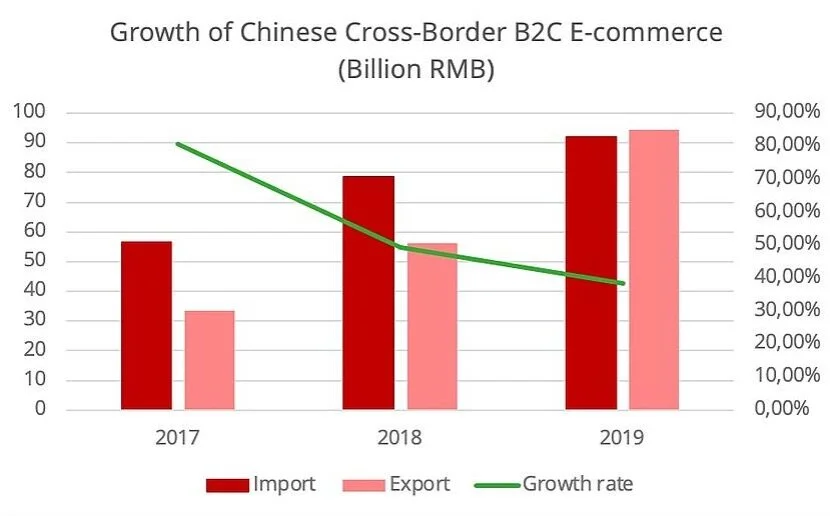

This plot shows the growth in B2C E-commerce in Europe area. It is evident that the E-commerce keeps growing in recent years, although the growth rate slows down. However, 80% growth rate of import and 83% growth of export have already proved that there is huge potential in the E-commerce in Europe. It can be seen that Europe is becoming the main market for China's e-commerce, which reflects the ever-strengthening trade relations between China and Europe when both China and Europe are being targeted by the protectionism from the United States.

此圖顯示了歐洲地區 B2C 電子商務的增長。 可以看出,電子商務近年來一直在保持增長,儘管增速有所放緩。 然而,80%的進口增速和83%的出口增速已經證明了歐洲電子商務的巨大潛力。由此可見,歐洲正在成為中國電商的主要市場,側面反映了在中歐都被美國的保護主義排擠的情況下,中歐之間不斷加強的貿易關係。

2

Changes in Amazon's Tax Declaration System

亞馬遜報稅政策的變化

Past Tax System for E-commerce

針對電商的舊政策Sellers on online marketplaces (e.g. Amazon) account for VAT at the point of sale

在線市場(例如亞馬遜)上的賣家在銷售點繳納增值稅Imports of goods less than €22 are exempt from VAT

不超過22歐元的小包裹享受增值稅免徵待遇Distance-selling thresholds

遠程銷售閾值VAT only applied to intra-community distance sales if annual turnover exceeds €35,000 for most EU countries (€100,000 for Germany, the Netherlands and Luxembourg)

如果在大多數歐盟國家的年營業額超過 35,000 歐元(德國、荷蘭和盧森堡為 100,000 歐元),增值稅則適用於歐盟範圍內的遠程銷售

Changes

變化Online marketplaces (e.g. Amazon) are the deemed supplier for VAT purposes in certain cases

將供應商品的在線市場/平台(例如亞馬遜)在特定情況下視為增值稅供應商Removes the need for sellers who use these marketplaces to account for VAT at the point of sale

免除了使用這些在線市場的賣家繳納增值稅的必要When these conditions are satisfied for B2C transactions in the EU, the online marketplaces will be the deemed the VAT supplier:

以下情況的B2C商品銷售,供應商品的在線平台將要承擔增值稅代扣代繳義務:Any company that is not established in the EU and has FBAs in the EU and sells goods in the EU (regardless of value)

任何未在歐盟成立但在歐盟擁有 FBA 並在歐盟銷售商品的公司(無論貨值多少)Any company that is not established in the EU and does not have an FBA in the EU and sells goods that do not exceed €150 in value

任何未在歐盟成立且在歐盟沒有 FBA 的公司,而且貨值不超過 150 歐元Any company that is established in the EU and does not have an FBA in the EU and sells goods that do not exceed €150 in value

任何在歐盟成立且在歐盟沒有 FBA 的公司,而且貨值不超過 150 歐元The VAT charged is based on the VAT rate in the country to which the goods were sold

歐盟增值稅代扣代繳是統一按照目的國的稅率(即買家所在地)進行代扣

Abolishing of Low-Value Consignment Relief

增值稅豁免政策取消Imports of goods less than €22 are no longer exempt from VAT

不超過22歐的小包裹7月後也需要繳稅All imported e-commerce goods are subject to VAT regardless of their value

所有的進口電子商務包裹無論貨件價值多少均需繳納應繳增值稅

Removal of distance-selling thresholds

棄用遠程銷售閾值Affects businesses that conduct intra-community distance sales

適用於公司成立地在歐盟境內,從公司成立地配送至其他歐盟國家/地區個人買家的銷售Uniform threshold of €10,000 per annum across all of the EU

整個歐盟的統一閾值為每年 10,000 歐元Does not apply to most Chinese e-commerce sellers

不適用於大部分中國電商The new threshold does not apply to sales outside the country where the company is established

新的遠程銷售閾值不適用於在公司註冊地址所在國家/地區境外進行的銷售The new threshold does not apply to sales that are affected by the new deemed VAT supplier rules

新的遠程銷售閾值不適用於在線平台代收代繳增值稅的銷售

3

Chinese E-commerce Businesses Moving to Ireland

中國電商移動至愛爾蘭

Misconceptions

誤解

Many Chinese e-commerce firms are drawn to Ireland as they believe it will be favourable for them tax-wise. This is because Ireland has a corporate income tax rate of 12.7%. However, this is a common misconception caused by two reasons. Firstly, the confusion between CIT and VAT. Secondly, the lack of understanding in the European Tax System and Amazon's tax declaration scheme.

許多中國電子商務公司都被愛爾蘭吸引,因為他們認為這對他們在稅收方面有利。這是因為愛爾蘭的企業所得稅率為 12.7%。然而,這是由兩個原因引起的常見誤解。首先,所得稅和增值稅之間的混淆。其次,對歐洲稅收制度和亞馬遜的納稅申報方案缺乏了解。

Firstly, although Ireland has a CIT rate of 12.7%, it is the VAT rate that is affected by the change in policy, and Ireland has a VAT rate of 23%, which is higher than countries such as France or Germany. This misconception was amplified by Chinese trade intermediaries encouraging the setting up of companies in Ireland due to its low CIT.

首先,雖然愛爾蘭的所得稅稅率為12.7%,但受政策變化影響的是增值稅稅率,愛爾蘭的增值稅稅率為23%,高於法國或德國等國家。 愛爾蘭較低的企業所得稅也給了中國貿易中介鼓勵客戶在愛爾蘭設立公司的原因,雖然這是個錯誤的原因,但依然加劇了這種誤解。

Secondly, most e-commerce firms do not have FBAs in Ireland. Rather, they have them in France or Germany. This means that they are not required to pay Irish VAT. However, they do have to apply for a VAT ID in the country their firms are incorporated in, and then apply for a VAT ID from the country where their FBAs located. Therefore, this makes setting up an Irish company even more undesirable, because of the difficulty in applying for an Irish VAT ID. The e-commerce firms would have to prove that their annual sales would exceed the threshold set by Irish tax authorities to be considered for a VAT ID. Considering that most Chinese e-commerce firms do not have FBAs in Ireland, do not mainly sell in Ireland, and do not use Irish bank accounts for their transactions, this makes it extremely difficult to show that their revenues will exceed the threshold. Therefore, it is extremely difficult for Chinese e-commerce firms to obtain an Irish VAT ID, if they choose to set up a company in Ireland.

其次,大多數電子商務公司在愛爾蘭沒有亞馬遜FBA倉庫。相反,他們的倉庫通常都在法國或德國。這意味著他們不需要支付愛爾蘭增值稅。但是,他們必須在其公司註冊所在的國家/地區申請增值稅號,然後從其 FBA 所在的國家/地區申請增值稅號。因此,這使得設立愛爾蘭公司更加不可取,因為申請愛爾蘭增值稅號很困難。電子商務公司必須證明其年銷售額將超過愛爾蘭稅務機關設定的增值稅識別門檻。考慮到大多數中國電商在愛爾蘭沒有FBA,也不主要在愛爾蘭銷售,也不使用愛爾蘭銀行賬戶進行交易,這使得他們很難證明他們的銷售額會超過門檻。因此,中國電子商務企業如果選擇在愛爾蘭設立公司,獲得愛爾蘭增值稅號是極其困難的。VAT vs. Company Income Tax

增值稅與所得稅的區別The payable VAT amount is calculated as the difference between output VAT amount (levied on the exportation of products, or when goods and services are sold to other businesses or consumers in general) and input VAT amount (levied on the importation of products, or when a business purchases VATable goods or services, usually included in the price). This tax is more relevant than CIT for Chinese e-commerce companies as these companies have accounts based in China.

增值稅應納稅額為銷項增值稅額(對產品出口徵收,或一般向其他企業或消費者銷售商品和服務時徵收)與進項增值稅額(對進口產品徵收,或企業購買應稅商品或服務,通常包含在價格中)。對於中國電子商務公司而言,這項稅收比 CIT 更重要,因為這些公司的賬戶位於中國。

4

TKEG Solutions - France and Germany

奕資方案 - 法國及德國

Chinese sellers prefer Amazon Seller Centrals in France and Germany, the two largest transit countries in the EU. If a company has warehouses in either France or Germany (i.e. if it is part of a French/German Amazon Seller Central), it must have a French or German tax number regardless of where in the EU the company is registered. France and Germany are also the countries that should be the most desirable location to register a company in, if Chinese sellers want to mitigate the impacts caused by changes in tax policy.

中國賣家喜歡法國和德國的亞馬遜賣家中心,畢竟這兩個國家是歐盟最大的中轉國。 如果公司在法國或德國設有倉庫(即,如果它是法國/德國亞馬遜賣家中心的一部分),則無論公司在歐盟的哪個地方註冊,它都必須擁有法國或德國的稅號。 如果中國賣家希望減輕稅收政策變化帶來的影響,法國和德國是最適合註冊公司的國家。

Advantages:

優勢:

The two recommended countries to register a company in are France and Germany, due to the reasons outlined below:

推薦註冊公司的兩個國家是法國和德國,原因如下:

Most Chinese sellers have FBAs in France or Germany, meaning that they already have a French or German VAT ID

大多數中國賣家在法國或德國都有FBA,這意味著他們已經擁有法國或德國的增值稅IDFrench or German VAT ID is required to incorporate a company in either country.

法國或德國的增值稅號是在法國或德國成立公司的必要條件

Relatively more economically developed

經濟比較發達Large European countries with a wide range of industries

擁有廣泛產業的歐洲大國Less likely to have Amazon seller accounts terminated due to reused company address

不太可能因重複使用公司地址而被終止亞馬遜賣家賬戶

Lower costs in the long run compared to Ireland with regards to company registration

從長遠來看,與愛爾蘭相比,公司註冊成本更低Ireland: requires annual payment for an EEA director / purchase of Section 137 Bond once every two years

愛爾蘭:需要每年向 EEA 董事付款 / 每兩年購買一次第 137 條債券From second year onwards, France and Germany will have an obvious cost advantage

從第二年開始,法國和德國將具有明顯的成本優勢

The advantage of already having a French or German VAT ID is that the ID is also required for incorporating a company in either of the two countries. Therefore, already having FBAs in France and Germany is an advantage for e-commerce firms wanting to set up companies there, since the process would be much less tedious. It is also much easier to provide evidence of meeting the revenue threshold, given that Chinese sellers have FBAs in the two countries and that France and Germany are major markets. Furthermore, German VAT threshold is way lower than Ireland.

已經擁有法國或德國增值稅號的優勢在於,在這兩個國家/地區中的任何一個國家成立公司也需要該稅號。 因此,對於想要在法國和德國設立公司的電子商務公司來說,已經在法國和德國擁有亞馬遜物流方案是一個優勢,因為申請過程會順利很多。 鑑於中國賣家在這兩個國家擁有亞馬遜物流方案並且法國和德國是主要市場,因此提供滿足收入門檻的證據也容易得多。 此外,德國的增值稅門檻遠低於愛爾蘭。

Registering in a larger and more developed EU country also ensures that the Amazon seller account would not be terminated due to reused company address. Since the reason behind Chinese sellers registering their companies in EU countries is to take control of their tax payments, choosing an EU country that is able to provide a sole address means a longer duration of control over their tax payments. Henceforth, the company can reap the long-term benefits from tax avoidance by taking control over its tax payments and utilising accounting practises regarding input and output VAT, allowing them to offset each other to minimise its tax payments. This would only lead to a tax payment of several hundred Euros in VAT every quarter, therefore maximising the company’s profits.

在更大、更發達的歐盟國家註冊還可以確保亞馬遜賣家賬戶不會因為重複使用公司地址而被終止。 由於中國賣家在歐盟國家註冊公司的原因是為了控制他們的納稅,選擇一個能夠提供唯一地址的歐盟國家意味著他們將會擁有更長的時間控制他們自己的繳稅。 今後,公司可以通過控制其納稅和利用進項和銷項增值稅的會計慣例從避稅中獲得長期利益,允許它們相互抵消以最大限度地減少納稅。 這只會導致每季度繳納數百歐元的增值稅,從而最大限度地提高公司的利潤。

Lower long run costs also make France and Germany more desirable destinations compared to Ireland. The annual payment for an EEA director or purchase of Section 137 Bond will be required, which will certainly outweigh the short-term gains of registering a company in Ireland caused by ease of registration process.

與愛爾蘭相比,較低的長期成本也使法國和德國成為更理想的目的地。 歐洲經濟區董事的年度付款或購買第 137 條債券的支出將是必需的,這些成本肯定會超過因註冊流程簡便而在愛爾蘭註冊公司的短期收益。

For comparison, the reasons behind the popularity of Ireland among Chinese e-commerce firms are outlined below:

相比之下,愛爾蘭在中國電子商務公司中受歡迎的原因概述如下:

Failure of Chinese e-commerce firms in distinguishing CIT from VAT

中國電子商務企業未能區分所得稅和增值稅Little to no documentation and capital contribution are required for registration

註冊時幾乎不需要文件及出資Short application timeline which lasts around 1-2 weeks

申請時間短,持續約 1-2 週

Since none of the three points are related to the long-term benefits of a company, the notion that Ireland is a desirable destination for Chinese e-commerce firms wanting to engage in tax avoidance is unjustified.

由於這三點都與公司的長期利益無關,因此認為愛爾蘭是中國電子商務公司想要避稅的理想目的地的觀點是不合理的。

Disadvantages:

弊端:

At the same time, there are also disadvantages associated with registering a company in France or Germany:

同時,在法國或德國註冊公司也有一些弊端:

Requires annual financial statements, VAT declaration and CIT declaration

需要年度財務報表、增值稅申報和所得稅申報Applies to both operating and non-operating companies

適用於運營和非運營公司Accounting fees will be at least 6,000RMB per year

會計費用至少每年6,000元人民幣

In Ireland, only an annual audit is required that costs approximately 2,500RMB per year

在愛爾蘭,僅需要年度審計,費用約為每年 2,500 元人民幣Capital contribution of around 2,000 Euros required for registration

註冊所需出資約2,000歐元No such requirement in Ireland

愛爾蘭沒有這樣的要求

Tedious registration process

繁瑣的註冊過程In Germany, a lot of document legalizations are required

在德國,需要做文件公證及雙認證In France, the capital contribution requirement makes registration more tedious for Chinese sellers due to foreign exchange controls in China

在法國,由於中國的外匯管制,繳納注資的要求使中國賣家的註冊更加繁瑣

However, despite these disadvantages, the benefits of registering a company in France or Germany outweigh the costs. This is because the advantages of Ireland failed to address the issues of the high cost of appointing a director who is an EEA resident and the greater probability of having the seller account terminated due to large number of company registrations in Ireland. The tedious registration process and more stringent requirements for documents in France and Germany will be relatively minor issues, especially if the company is planning to operate in the European market for an extended duration of time.

然而,儘管有這些缺點,在法國或德國註冊公司依然利大於弊。 這是因為愛爾蘭的優勢未能解決任命一位歐洲經濟區居民董事的高成本的問題,或者由於大量公司在愛爾蘭註冊而導致賣方賬戶更有可能被終止的問題。 如果公司計劃在歐洲市場長期運營,法國和德國繁瑣的註冊過程和更嚴格的文件要求將是相對較小的問題。

5

Reverse Charge Mechanism

反向徵收機制

In the case of most B2B transactions, the VAT burden is usually on the seller. However, reverse charge differs from regular VAT settlement in that it will be the buyer declaring VAT in certain B2B transactions. As the reverse charge mechanism shifts the responsibility of VAT declaration from the seller to the buyer, this provides opportunities for the buyer to submit VAT returns without requiring the seller to register as a VAT payer in the country to which the goods or services were supplied.

在大多數 B2B 交易的情況下,增值稅負擔通常由賣方承擔。 但是,反向徵收機制與常規增值稅結算不同,因為它是買方在某些 B2B 交易中申報增值稅。 由於反向徵收機制將增值稅申報的責任從賣方轉移到買方,這為買方提供了提交增值稅申報表的機會,而無需賣方在提供商品或服務的國家/地區註冊為增值稅納稅人。

Reverse charge usually apply to B2B transactions that are services-based, the general prerequisite is that the buyer must have be VAT-registered. In practise, a seller would indicate on the invoice to a buyer that reverse charge applies to this transaction. The buyer then have to declare both its input VAT and output VAT as if the buyer supplied the goods or services themselves, both values will cancel each other out but tax authorities can still capture the transaction that took place. The VAT rate on the seller side should be considered as if the seller was operating in the country where the transaction took place. In other words, there would be no output VAT charged by the seller under a reverse charge scenario, the transaction itself would have no VAT applied but the buyer would be responsible for calculating both input and output VAT on its VAT return.

反向徵收通常適用於以服務為基礎的 B2B 交易,一般先決條件是買方必須進行增值稅登記。 在實踐中,賣方會在發票上向買方表明反向徵收適用於該交易。 然后買方必須申報其進項增值稅和銷項增值稅,就好像買方為自己提供商品或服務一樣,這兩個稅將相互抵消,但稅務機關仍然可以捕獲發生的交易。 賣方的增值稅稅率應視為賣方在交易發生的國家/地區開展業務。 換句話說,在反向徵收的情況下,賣方不會收取銷項增值稅,交易的金額將不會包括增值稅,但買方將負責在其增值稅申報表中計算進項和銷項增值稅。

Article 196 of the VAT Directive implies that a supplier providing services to a VAT-registered customer in another EU member state without being established there will not charge any VAT on the invoice. Instead, the customer will reverse charge the transaction, this is made possible because the place of supply is where the customer is established. However, there are exceptions when reverse charge does not apply. This is because for some services the place of supply is not where the customer is established. Here are some examples:

增值稅指令第 196 條指示,向在另一個歐盟成員國註冊增值稅的客戶提供服務但未在那裡成立的供應商不會在發票上收取任何增值稅。 相反,客戶將反向徵收交易費用,這是可能的,因為供應地點是客戶成立的地方。 但是,不適用於反向徵收的情況也有例外。 這是因為對於某些服務,供應地不是客戶所在的地方。 這裡有些例子:

Immovable property

不動產The place of supply is where the property is located.

供應地取決於房產所在的地方。

Passenger transport

客運The place of supply will be located where the transport takes place, usually in a variety of locations.

供應地點將位於運輸發生的地方,通常位於不同的地點。

Catering

餐飲服務The place of supply is where the catering services are rendered.

供應地是提供餐飲服務的地方。

For Chinese e-commerce firms that have registered a company in an EU country and are engaged in B2B transactions, the reverse charge mechanism could potentially apply to them. However, there are two points worth noting. Firstly, most Chinese e-commerce firms sell goods rather than services. Secondly, each individual EU country is free to impose additional conditions, which could make things complicated for Chinese sellers. Both of which means it would be unlikely that Chinese e-commerce firms would be sending invoices to buyers indicating that this is a reverse charge transaction. However, there are two scenarios involving reverse charge that apply the most to Chinese sellers. The first one being intra-community acquisition, the second one being domestic reverse charge for non-established suppliers.

對於在歐盟國家註冊公司並從事 B2B 交易的中國電子商務公司,反向徵收機制可能適用於他們。 但是,有兩點值得注意。 首先,大多數中國電子商務公司銷售的是商品而不是服務。 其次,每個歐盟國家都可以自由施加附加條件,這可能會使中國賣家的情況變得複雜。 這兩者都意味著中國電子商務公司不太可能向買家發送發票,表明反向徵收適用於此交易。 但是,有兩種涉及反向徵收的情況最有可能適用於中國賣家。 第一種是於歐盟境內取得貨物,第二種是對非成立供應商的國內反向徵收。

Intra-community acquisition refers to the acquisition of moveable goods by a business in one EU member state from a business in another member state, which could take place between a European buyer and a Chinese seller. In these transactions, the purchaser making the intra-community acquisition is obliged to declare both the input and output VAT.

歐盟境內取得貨物是指歐盟成員國的企業從另一成員國的企業收購可移動貨物,這可能發生在歐洲買家和中國賣家之間。 在這些交易中,進行境內取得貨物的買方有義務同時申報進項和銷項增值稅。

Domestic reverse charge for non-established suppliers refers to reverse charge being imposed on domestic supplies of goods and services, and takes place under the conditions that the seller is not established in the country the buyer is located in and that the transaction takes place in the country of seller.

非成立供應商的國內反向徵收是指對國內供應的商品和服務進行反向徵收,發生的前提是賣方不在買方所在的國家/地區成立,並且交易發生在賣方所在的國家/地區。

6

Reference

參考

Christopher K Johnson, “President Xi Jinping’s ‘Belt and Road’ Initiative: A Practical Assessment of the Chinese Communist Party’s Roadmap for China’s Global Resurgence”, CSIS Report, 28 March 2016, https://www.csis.org/analysis/president-xi-jinping’s-belt-and-road-initiative.

Youli Yin,“中歐班列國際抗疫立新功”,人民網 ["China-EU Railway Makes New Contributions in International Anti-Pandemic Efforts". (2020, May 5). Retrieved from people.cn: http://world.people.com.cn/n1/2020/0509/c1002-31703112.html]

外長點贊中歐班列:歐亞大陸之間名副其實的“生命之路”,中國新聞網 ["Foreign Minister Praises China-EU Railway: A Veritable "Road of Life" between Europe and Asia". (2020, May 26). Retrieved from chinanews.com: http://www.chinanews.com/gn/2020/05-26/9195330.shtml]

"中歐班列奔向黃金時代”,中國經濟網 ["China-EU Railway Approaches Golden Age". (2017, May 25). Retrieved from China Economic Daily: https://web.archive.org/web/20170731150614/http://m.hexun.com/gold/2017-05-25/189340884.html]

“打造巴爾幹絲綢之路,中國“一帶一路”前進希臘”,地球圖輯隊 ["Building the Balkan Silk Road, China's OBOR Advances to Greece". (2019, November 13). Retrieved from dq.yam.com: https://dq.yam.com/post.php?id=11834]

“巴爾幹絲綢之路:復興一個地區?”,進出口經理人 ["The Balkan Silk Road: The Rejuvenation of a Region?". Retrieved from Imp-Exp Executive: http://www.tradetree.cn/content/6325/4.html]

【歐洲時報】CCG報告:中國B2C跨境電商“出海”加速,向“一帶一路”沿線延伸 ["CCG Report: Chinese B2C Cross-Border E-Commerce Companies Accelerate Going Overseas, along the OBOR". (2021, June 24). Retrieved from Center For China & Globalisation: http://www.ccg.org.cn/archives/64240]